Contextualizing the State of the Cloud for Indian Founders

Contextualizing the State of the Cloud for Indian Founders

What Indian SaaS Founders should take away from Bessemer's State of Cloud 2022

Bessemer recently released their annual State of the Cloud. This is an annual reflection on where the Cloud stands today, how the past year was, and what we have to look forward to. While this report is global in nature, we wanted to contextualize what this means for Indian SaaS founders building for global markets. You can read the entire report at https://www.bvp.com/atlas/state-of-the-cloud-2022.

First off, let’s address the elephant in the room.

The Euphoria of 2021

In a twist of the classic Murphy’s law — Whatever could go right, did go right!

The total public cloud market capitalization reached a peak of $2.7 trillion in November ‘21 from $1 trillion in Feb ‘20. Tech IPOs in 2021 brought in $142.2 billion with some great companies like Toast, Procore, Hashicorp, Freshworks, Amplitude and SentinelOne, Gitlab, and others going public. M&As on the other hand made up $1.24 trillion, where the likes of Afterpay, Mailchimp, Mandiant, etc. were acquired by Strategic Investors.

However, coming back to the present, headlines are now focused on the slowdown, the number of months without unicorns, etc. In fact, The BVP Nasdaq Emerging Cloud Index is down to its 2020 levels, dropping over 40% in value. As of May 2022, the cumulative market capitalization of the public cloud is approximately $1.4 trillion.

💡 But just as the saying by Benjamin Graham goes, “In the short term, the market is a voting machine; In the long term, the market is a weighing machine”.

This drop has been disconnected from business performance as this set of companies is still growing by an average of 41%, with a 71% average gross margin and 45% average efficiency score.

So it seems like it’s time to go back to basics and remind ourselves why we are still firm believers in the power of the SaaS businesses and the cloud.

In this piece, we’ll go through

The macro-environment that’s going to drive the next phase of growth,

Who’s, Why’s, and How’s of Cloud Adoption and Emerging GTM Motions

What all this means for Indian SaaS founders

And finally, what takeaways should we take from this

Macro Drivers for the Cloud

1. Tech hosted on the cloud has become the backbone of businesses

Innovations in Bandwidth, Data, APIs, ML, and AI from Image Recognition to Language Generation, have been the major drivers behind this SaaS model of selling.

Despite all this, the Public cloud spends still only makes up 10% of the total $4 trillion total IT spend across the globe. North America, where the public cloud contributes 15% of total cloud spend, makes up 55% of all the global public cloud spend.

However, other geographies are still lagging. Europe, which makes up 26% of the global cloud spends, only spends 10% of its IT budget on the cloud. LATAM, APAC, and MENA are still in the very early days, combining to contribute less than 20% to the global cloud spend, making up less than 10% of the geographies’ total IT spend.

These IT spends will make their way into a hybrid cloud infrastructure and provide major tailwinds to cloud spend in the next decade.

2. Vertical SaaS is still in very early days

Low cloud penetration rates across different industries within the United States alone illustrate just how far the cloud economy has left to go. The low cloud penetration is evidenced by low market share capture by the leading vertical cloud players:

Restaurants (860k restaurants) — Toast, the restaurant management SaaS, is only in 6% of U.S. restaurant locations.

Public Transit ($60 billion TAM)— Optibus, the cloud-native AI platform that makes public transportation smarter, better, and more efficient, has reached less than 1% of the total public transit software market.

Home Services (900K businesses) — ServiceTitan, a leading vertical SaaS for home services, penetrated 1% of its core TAM of 900,000 home services businesses.

Other verticals such as auto repair with Shopmonkey (260k auto repair shops) and laundry services with Cents (80k laundry services) have seen a 2% penetration.

Vertical SaaS continues to attract customers as they provide specific solutions that horizontal SaaS counterparts can’t cater to. We are currently observing an exaggerated version of this trend play out in the Supply Chain space:

Disruptions like China blocking exports, the Evergiven saga

,and the Ukraine war, have meant that the environment is ripe for the adoption of SaaS products to help manage the global supply chain and increase efficiency.Over 90% of Fortune 500 C-suites report having plans to increase resilience in their supply chain this year, and yet 50% of U.S. importers still use spreadsheets to manage their business. These issues are going to provide massive tailwinds to investments in this space.

Low penetration in vertical industries, when coupled with the emergence of a low-touch model of selling is expected to provide a massive boost to startups building in these spaces.

3. On the Cloud Infrastructure side of things

The increasing sophistication of the Cloud Infrastructure has meant that even sensitive data like security logs and financial records are now stored in the cloud. The pace of development of the cloud infrastructure has allowed early adopters of the cloud to shift more data from on-prem to the cloud to manage their business more efficiently

The On-Prem market is also being chipped away by Virtual Private Clouds as slow adopters of the cloud are using containerization technologies like Kubernetes to leverage the cloud infrastructure without storing their data on the public cloud.

The above two themes have also led to an emergence of a layer of infrastructure that’s helping traditional industries with legacy software to transition some or all of their data to the cloud.

Ultimately, these trends help highlight the pace of technological advances along with the road left ahead of us, as the cloud continues to consume all of enterprise IT.

Who’s, Why’s, and How’s

Who are the end-users leading this growth, where are these structural tailwinds, and how the GTM motions are adapting to this?

Who — Increasing IT Spends by CIOs

Stronger SaaS products, business models, and delivery methods drive increasingly strong enterprise demand for cloud products. We can see this as CIOs globally are pushing to increase their company’s IT spend. In Q4 ‘20, 44% of CIOs expected to increase their IT spends while only 12% were expected to reduce it. By Q4 ‘21, this moved to 49% and 8% respectively. Mind you, both of these are numbers from a post-pandemic world!

Thus, it’s not surprising to see enterprise demand for IT continue to rise, with the cloud still clearly on track to become the largest spend category within all of IT.

Why — Structural Macro Tailwinds

There are more than a billion knowledge workers in the world today. Yet there are only 20 million developers in the world today building software. We expect more creative abilities to be put in the hand of these knowledge workers. Some of the trends in the market today are:

Empowering Creators — Today there are around 1.1 billion freelancers around the world who leverage creator and builder tools to monetize their talents. Over 50% of younger generations suggest that they are likely to freelance in the future.

Software is going to play a crucial role in enabling this. SaaS solutions are helping “arm the rebels,” as Shopify’s Founder and CEO Tobi Lutke once said. Creator platforms like Canva, Patreon, and Substack are leading the way.

Cloud Software enabling Hybrid Work — A post-covid world has led to an increased focus on productivity and most of the changes we’ve made to our lives are here to stay.

The shift toward a hybrid work environment and structural issues like The Great Resignation has put a spotlight on Employee productivity. This has become top of the mind for companies as we are seeing structural changes to the labor market.

One of the ways has been the unbundling of traditional enterprise software stacks. This suite of tools is now empowering a wider class of workers with a focus on empowering them to move towards higher-value work.

Examples of this are, horizontal platforms like Hibob and Papaya Global which are supporting businesses with HR management and payroll; Tools like Productboard and Demostack which are helping optimize GTM motions and products.

How — Emerging GTM channels

Cloud software has attained a certain level of maturity we can now observe consumer-style GTMs such as cloud marketplaces and indirect monetization.

Cloud Marketplaces — Cloud Marketplaces have emerged as an upcoming channel to sell software. 2021 saw marketplace transactions grow an estimated 70% to $4 billion, which is 3x faster growth than the public cloud at large.

According to cloud marketplace platform Tackle.io, Cloud Marketplaces are expected to grow at a 88% CAGR from 2022 to 2025, growing from $8 billion in GMV in 2022 to $50 billion in GMV by 2025.

Furthermore, 45% of the Cloud 100 companies were actively selling on at least one cloud marketplace in 2021. By 2024 we can expect 80% of Cloud 100 companies will be actively selling through these cloud marketplaces. Companies’ sales, marketing, and communications, apart from infrastructure SaaS providers have leveraged the marketplace as a sales channel

This adds yet another channel to sell to enterprises and helps solve the classic Indian founder problem of how to get your first customers in the US

Indirect Monetization — The proliferation of APIs has led to a boom in businesses monetizing customers through indirect ways.

Businesses that we’ve seen successfully lean into indirect monetization so far include the likes of Ambrook, Basicblock, Brex, Built, Cents, Coast, Fresha, Gloss, Genius, Lasso, Miter, MVMNT, Mycarrier, Ramp, Wrapbook, among others.

Some companies are jumping to completely free software as a lead generation tactic to capture more lucrative indirect monetization streams.

Either way, indirect monetization is an extremely effective way to build a business, and given the increasingly competitive SaaS markets, this strategy is becoming table stakes.

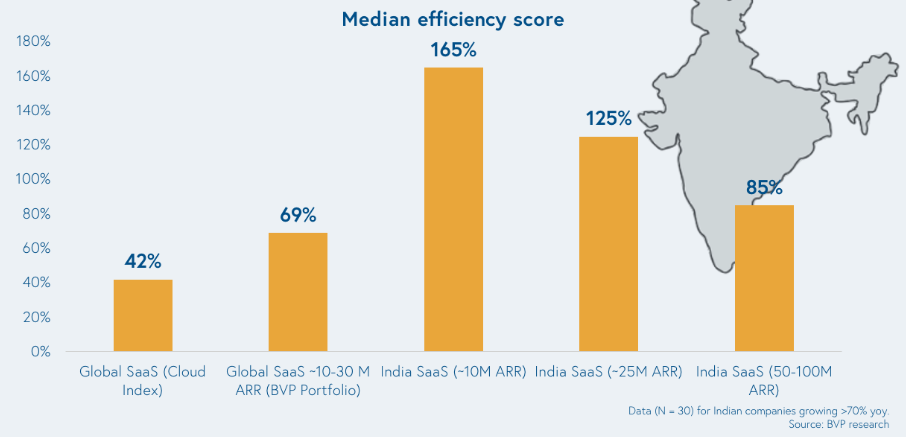

So where does India fit into all this

Above is Bessemer’s chart on efficiency scores* across Global Public SaaS, Bessemer’s early-stage portfolio, and Indian SaaS companies across the early and growth stages.

Interestingly, Indian early-stage companies have shown extremely high efficiency in adding new revenue. One major factor for this has been the focus on adding new use cases in their products at a much earlier point in their lifecycle compared to their global counterparts.

Early indicators also show that Indian SaaS businesses demonstrate faster payback cycles and are more efficient in their ability to get to $100 million ARR with less than $100 million in equity capital.

*Bessemer Efficiency Score is a measure of capital efficiency that tracks net new ARR against net burn for a given period. This metric showcases the incremental ARR dollars added for every dollar of burn, effectively measuring a company's spending habits

Benchmarking India against other geographies

One very interesting point out of this state of the cloud was that Indian SaaS has to achieve higher benchmarks compared to their European Counterparts just due to the competitiveness of the ecosystem in India and its inherent efficiency (as seen in the graphic above). A company that is in benchmarking highly in terms of average growth in Europe would not benchmark highly against its Indian counterparts. This can also be seen in the graphics below.

Most best-in-class SaaS companies have approximately 60-70% sales efficiency at $10 million-$30 million ARR. As these companies grow, efficiency trends down to 30-40% by the time they reach scale (e.g., Rule of 40).

However, when we look at most Indian SaaS companies, they run at 80-100% or more sales efficiency, even up to $100 million in ARR. With these numbers, most Indian SaaS companies will have the ability to break even at around $10 million of ARR and will only need capital for achieving hyper-growth.

What can we take away from all this

We don’t want to get into prognostications on where the market will go.

But what we do know is that revenues are the building blocks on which valuations and fundraising are based. With the vast untapped markets that remain and trends in cloud adoption and GTM strategies highlighted above and keep building.

As for the state of India SaaS. We’ll just leave this here:

India SaaS has proven its structural advantages by building efficient SaaS products and businesses that benchmark well against their global counterparts.

The next wave of India SaaS will be able to take advantage of these new GTM models and the efficiencies to do better than the current stalwarts.

We at Fortytwo are particularly excited about what’s happening in this space. We know building companies can be hard. Especially if it is about taking your company global. If you are building an Enterprise Tech or SaaS company building for global markets, drop us a note at deepthought@fortytwo.vc.

*Most stats are taken from Bessemer’s State of the Cloud 2022. Refer to https://www.bvp.com/atlas/state-of-the-cloud-2022 for an exhaustive list of sources.