How much funding does your SaaS startup actually need?

How much funding does your SaaS startup actually need?

The last decade has seen a tremendous increase in VC funding and SaaS companies did not shy away from this gold rush. In fact, VC investments just in India grew 4-fold in a year and hit a record high of $38.5 billion in 2021!!

The increased funding activity in the last decade or so, begs the question: Whether more funding means more growth?

This sounds counterintuitive, but, more funding does not always equate to more growth or market capitalisation! I have tried to illustrate the previous statement in this article and have broken it down into the following three parts:

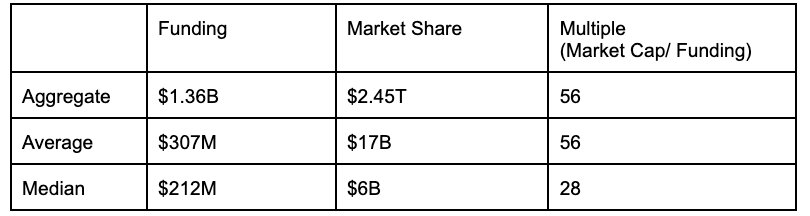

First, we took inspiration from Don’t Overdose on VC: Lessons from 166 startup IPOs where they analysed the 166 Tech IPOs since 2000 to see how VC funding affected their growth. We have conducted a similar exercise but focused purely on SaaS/Cloud companies. We have compiled data on eighty SaaS companies and the results are very identical.

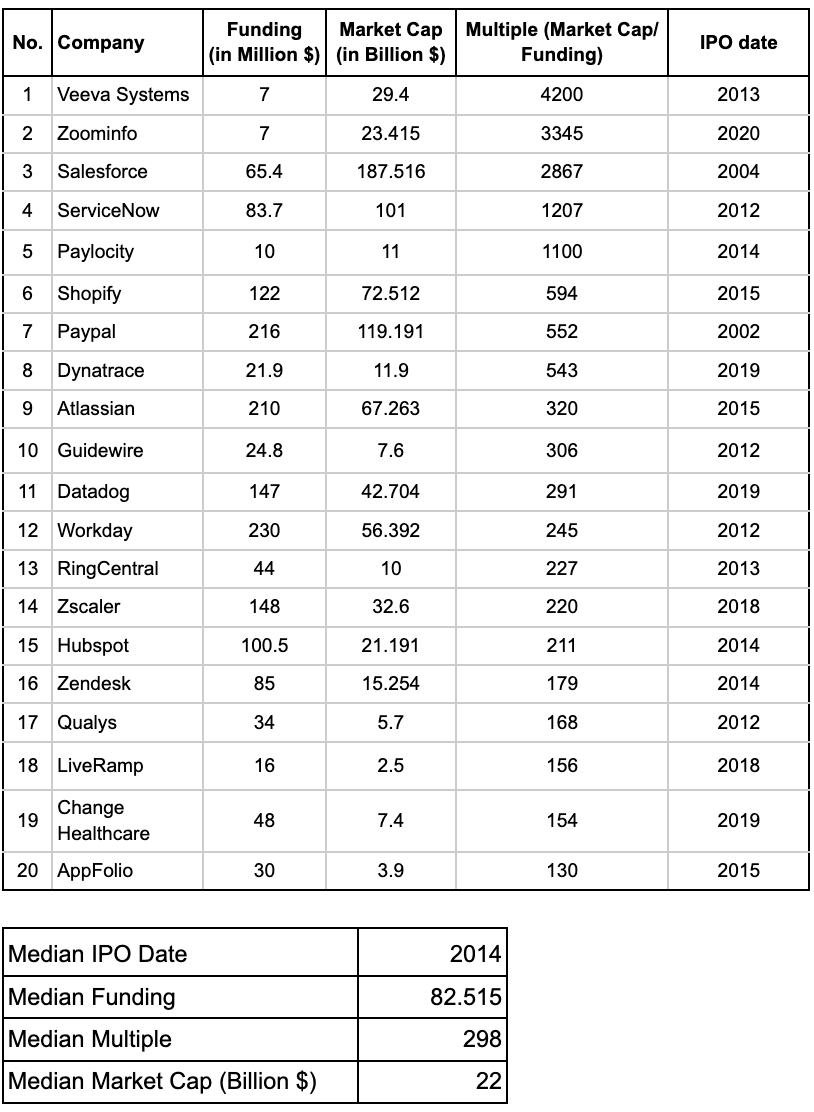

Second, we look into the company with the highest Multiple, and how it achieved a market capitalisation of $ 29 Bn with funding of just $ 7Mn, a x4200 Multiple!

Third, we look into the parameters a startup needs to consider to reach appropriate funding ask.

I. Reasons, why you don’t, need much VC funding

If funding is equated to growth or more market capitalisation then we can make two statements:

Statement 1: Most funded companies would be the most valuable, or at least their Multiples would be similar to that of the most valuable companies. (Multiple here is Market Cap/Funding. Higher the Multiple - higher the return on investment made.)

Statement 2: Most funded companies should have the highest Multiple. Discussed in I.A.

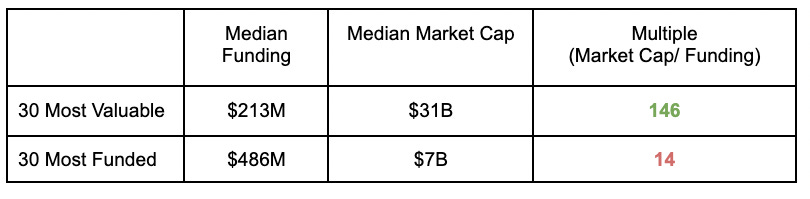

Looking into the first statement and comparing the most valuable and most funded public SaaS companies we have found the following:

The median Market Cap of the thirty most valuable Public SaaS companies was ~4X that of the thirty most funded ones, while median funding for the latter was more than 2X.

The differences between the Multiples are even more astounding! Most Valuable companies had 10X the Multiple for most funded companies.

Furthermore, the most-funded SaaS companies even fared lower in Market Cap and Multiple when compared to the average and median of all eighty SaaS companies on the list.

The above three points illustrate how the most funded SaaS companies do not seem to have additional leverage for higher market capitalisation or Multiple generation compared to the most valuable or even the average and median of the listed companies.

We will, therefore, look at the second statement, to see if the companies with the highest Multiples require much VC funding.

I.A. High Multiple companies need not be most funded

When looking at the best-performing companies, i.e. companies with high Multiples, there could be a couple of assumptions made.

Assumption 1: High Multiples were recorded before this decade when VC activity was lower. With more VCs in the market now, one could assume that VCs are competing to invest and hence sometimes invest at lower Multiples.

However, the reality is quite different. The companies with the highest Multiples as seen above are mostly from the last decade, with the median date of such companies going public being 2014. Hence, a high Multiple observed by companies is not related to external pressures like that of the heightened funding activity.

Assumption 2: High Multiples are observed due to higher funding.

The companies on the list had median funding of $82 Mn. This amount is significantly lower than the median funding of the entire 80 companies, i.e. $212 Mn. Hence, you don’t need too much funding to achieve those high Multiples.

Assumption 3: High Multiples are observed at lower market capitalisation, and higher investments would be required to achieve a higher market cap.

Again, this is untrue, high Multiple companies on the above list had a median market cap of $22 Bn compared to that of just $ 6Bn for the entire 80 companies. Therefore, a higher market cap is possible with a high Multiple.

Negating the three assumptions above establishes that creating a successful SaaS company with a high market cap and high Multiples is possible with prudent VC funding. And also proves that the most funded companies do not necessarily translate to the most valuable companies. The next question naturally is what do high Multiple companies do so well?

II. Achieving High Multiples.

We go over Veeva, a company with the highest returns on investors’ money. Veeva has a market capitalisation of $ 29 Bn and was able to achieve it with just $ 7 Mn in funding!

We, therefore, look into what were the catalysts that lead to such great returns. The answer is pretty simple, illustrating the importance of clear GTM strategies and proper execution.

Veeva went public in 2013, and in 2014, the company estimated its TAM to be ~ $5 billion. 8 years later Veeva has doubled its TAM. The reasons behind this increase are the following:

Adding more products: Veeva continues to launch new products, with MedTech CRM being their latest offering.

Land and Expand Strategy: Increasing the number of products alone isn’t enough. Veeva continues to upsell its customers on the new products it develops. To illustrate this, the number of products per customer continues to increase. And the number of customers with a higher number of products is increasing at a higher rate compared to customers with a lesser number of products. This Indicates, Veeva’s success in land and expansion strategy and also its product stickiness.

Improving services: Veeva consistently managed to keep an NRR in the 120% range over the last 6 years.

Industry Tailwinds: The Life Sciences Industry is growing at a 6% CAGR. Additionally, the global population will grow an additional 2 billion in the next 30 years along with the median age going from 35 years to 37 years in the same timeline. These two tailwinds will increase per capita healthcare spending to around 35%.

Profitable Business: Veeva has two revenue streams: a) Subscriptions for ~ 80% of revenue, and b) services for the rest ~ 20%. The gross margin on subscriptions is a healthy 75% and on services is 35%. This has meant that the net profit percentage Margin has been over 20% in the last few years.

III. What’s an appropriate amount of Funding?

In the above two sections, we dwelled on the market data of high performing SaaS companies and their fundings & valuations. The above two sections guide us on the kind of Multiple to aim for. However, evaluating the appropriate amount of funding cannot solely rely on external benchmarks. Externals benchmarks are just that, an ideal goal post. As a founder, you have to focus on raising an appropriate amount based on your company’s internal requirements.

Marc Andreessen’s blog post provides us with a simple framework on how to go about evaluating your need for funding. Condensing the blog post here, Marc rightly suggests that funding is determined based on the stage that the start-up is in:

Before Product-Market fit or

After Product-Market Fit.

For a company before product-market fit, the company should raise “enough” funding to reach the PM fit. And for a company that has already reached PM fit, it should raise “enough” money to exploit the opportunity.

Here, “enough” includes the following:

Money to achieve the said goal as per your company stage.

Additional money to counter expected but unanticipated setbacks: like product failing, lead engineer leaving etc.

Additional money to cushion unexpected and unanticipated setbacks, for example, the Pandemic, Ukraine-Russia war etc.

Additional money in the case your next round gets delayed.

By considering the four parameters the company should be able to reach an ask that would provide enough runway to reach the PM fit or exploit the opportunity to the maximum!

Building B2B Tech for Global Markets?

We know building companies can be hard. Especially if it is about taking your company global. If you are building an Enterprise Tech or SaaS company building for global markets, drop us a note at deepthought@fortytwo.vc